Last Updated on June 18, 2026 by Taya Ziv

In January, a company called Humans& raised $480 million. Not a Series C. Not a growth round. A seed round, the first money in, for a company that was roughly four months old. Its founders had come from Google, Anthropic, OpenAI, xAI and Meta, and that pedigree alone was apparently worth nearly half a billion dollars before they had shipped much of anything anyone could use.

If you are a normal founder, the kind without four ex-frontier-lab researchers on your cap table, a headline like that makes you feel two things at the same time. One, that money is everywhere right now. Two, that none of it seems to be coming to you. Here is the uncomfortable part: both feelings are correct, and the gap between them is the single most important thing happening in startup funding this year.

What actually happened

Let me give you the real numbers, because the headline version is misleading on purpose.

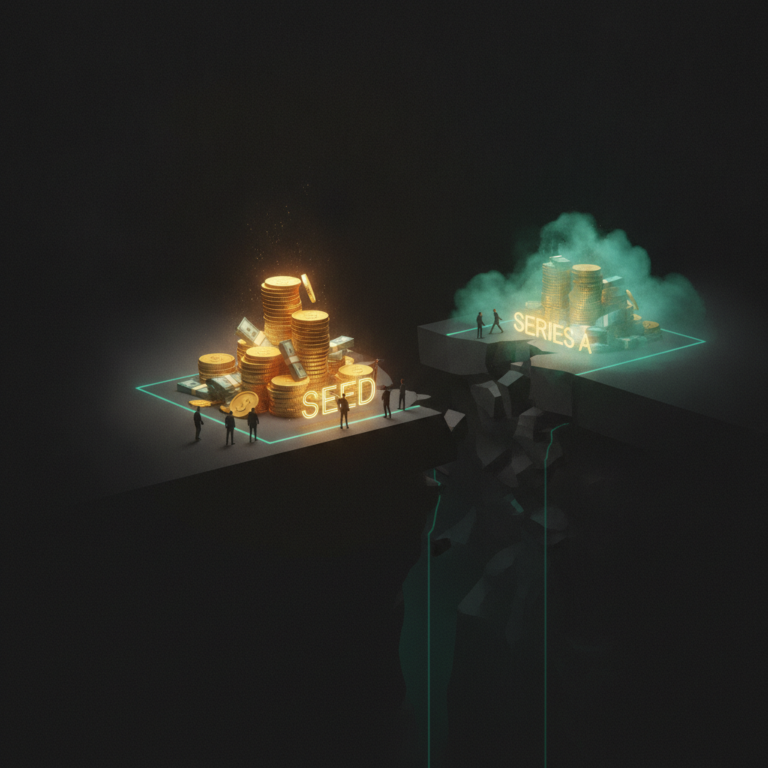

According to Crunchbase, more than 40% of all the money that went into seed and Series A rounds in 2026 went into rounds of $100 million or more. In the US it was over half. Sit with that for a second. The earliest, riskiest, supposedly smallest stage of startup investing is now a place where a coin flip’s worth of the capital lands in giant checks. Humans& got its $480 million seed. Ricursive Intelligence raised a $300 million Series A at a $4 billion valuation. Merge Labs, the brain-computer startup tied to Sam Altman, reportedly locked up a $252 million seed. These are not Series B companies dressed up. They are first and second checks, sized like exits.

So when you read that early-stage funding is booming, it is technically true and almost completely useless to you. The boom is a couple dozen enormous rounds going to AI labs founded by famous people. It is not a thousand normal rounds going to founders like you. It is the same concentration we watched when three hundred billion dollars of Q1 venture capital effectively funneled into a handful of companies, just pushed all the way down to the seed stage.

Now here is the part that should actually worry you, and it has nothing to do with the giant rounds. While the dollars pile up at the top, the bridge that every normal startup has to walk across, seed to Series A, is quietly washing out. Depending on whose data you read, somewhere between 15% and 24% of recent seed-funded companies are making it to a Series A within two years. For the seed classes of 2018 to 2020, that number was closer to 30%. For most of the last decade, raising a seed meant you had roughly a one-in-three shot at the next round. In 2026 it looks more like one in six.

Why your fundraising plan is probably broken

The mistake almost every founder is making right now is reading “record funding” and quietly assuming the ladder still works the way it did. Raise a seed, build for eighteen months, raise a Series A, repeat. That ladder is missing a rung, and nobody sent a memo.

The bar to clear at Series A did not just creep up. It roughly doubled. The going expectation in 2026 to raise a credible A is something like $2 to $3 million in real annual recurring revenue, growing two to three times year over year, with retention that does not leak out the bottom. A median seed today is around $4 million on a $15 million post-money valuation. A median Series A is around $10 to $12 million on a $45 million valuation. The valuation step-up between them barely moved, but the amount of proof you need to earn it got far heavier. As one investor put it this year, the money is back but the fantasy is out.

And the reason is the thing I keep coming back to in almost everything I write lately. Building got cheap. When your next real competitor is one person with a laptop and a weekend, a polished deck and a slick demo prove nothing, because anyone can produce them in an afternoon now. So investors stopped paying for potential and started paying for proof. A seed used to buy you permission to go figure it out. Now the Series A is the test of whether you actually did, and most companies are failing the test, or never getting to sit it.

The take, and where I might be wrong

Here is my honest read. The dangerous lie of 2026 is not “you can’t raise money.” You can. The lie is that you can raise a seed round on a good story and safely assume the Series A will be waiting for you when the runway gets thin. The math says it won’t be, for about five out of six of you.

So the move is almost the opposite of what the headlines push you toward. Raise your seed round as if it is the last outside money you will ever touch. Not because that is certain, but because planning for it is the only version of this where you stay alive if the bridge is out. Most founders treat a seed as runway to reach a Series A. Treat it instead as runway to reach a business.

Now let me argue against myself, because I could be reading a slow market as a dead one. Maybe these graduation numbers look brutal mostly because the 2023 and 2024 seed cohorts simply haven’t had enough time yet, and a chunk of them will still raise an A, just later than the old timeline. Fair. And maybe the mega-round concentration is an AI-lab quirk that doesn’t really touch a normal SaaS company’s odds at all. Also fair. I’m not certain the cliff is as steep as the worst numbers suggest. But notice that even the optimistic version leaves you in exactly the same spot tactically: the A is slower and harder than you planned for, so plan for the cliff and be pleasantly surprised if there turns out to be a bridge. The cost of being wrong in that direction is almost nothing. The cost of being wrong the other way is your company.

What to actually do about it

Stop benchmarking yourself against the $480 million seed. That is a different sport with different physics, and watching it will only make you raise too much, spend too fast, and build for a Series A that statistically isn’t coming.

Instead, pick a target that gets you to default-alive on the money you can actually raise. Before you take the check, know the number that makes you not need the next one: the revenue, the burn, the runway. Then build straight at it. This is the same logic behind the 90-day revenue rule that’s quietly replacing MVP culture, and it has never mattered more than it does now. Get to your version of undeniable, call it $2 million in ARR that grows, before you go raise the A, not after, and not as the thing the A is supposed to fund.

Measure progress in revenue and retention, not in vanity metrics that look great in a deck and mean nothing in a diligence call. If you are going to run low, run low slowly: cut burn early, extend runway, and give yourself the option to keep going without a round. And here is the part founders hate to hear. If the Series A never shows up and you’ve built a small profitable company instead, that is not a failure. That is a fine outcome, and increasingly it is the outcome that makes investors want to fund you anyway.

The headlines aren’t about you

The funding news for the rest of this year will keep telling you it’s the best environment for startups in ages. For about a dozen companies a quarter, it genuinely is. For everyone else, the smartest thing you can do is stop reading those headlines as though they describe your situation. They don’t.

Raise what you can. Then build like the next round doesn’t exist, because for most founders, on the timeline they expected, it doesn’t. If the Series A shows up, wonderful. If it doesn’t, you’ll have quietly become the founder who didn’t need it. Which, after all this, turns out to be the only kind everyone actually wants to back.